Sen. Taylor & TLR Can’t Defend Insurance Immunity Act. So, They’re Attacking Us.

Sen. Larry Taylor and his allies at TLR want to distract attention from the terrible impact SB 1628 – the Insurance Immunity Act – would have on Texas families and businesses by resorting to direct attacks on Texas Watch.

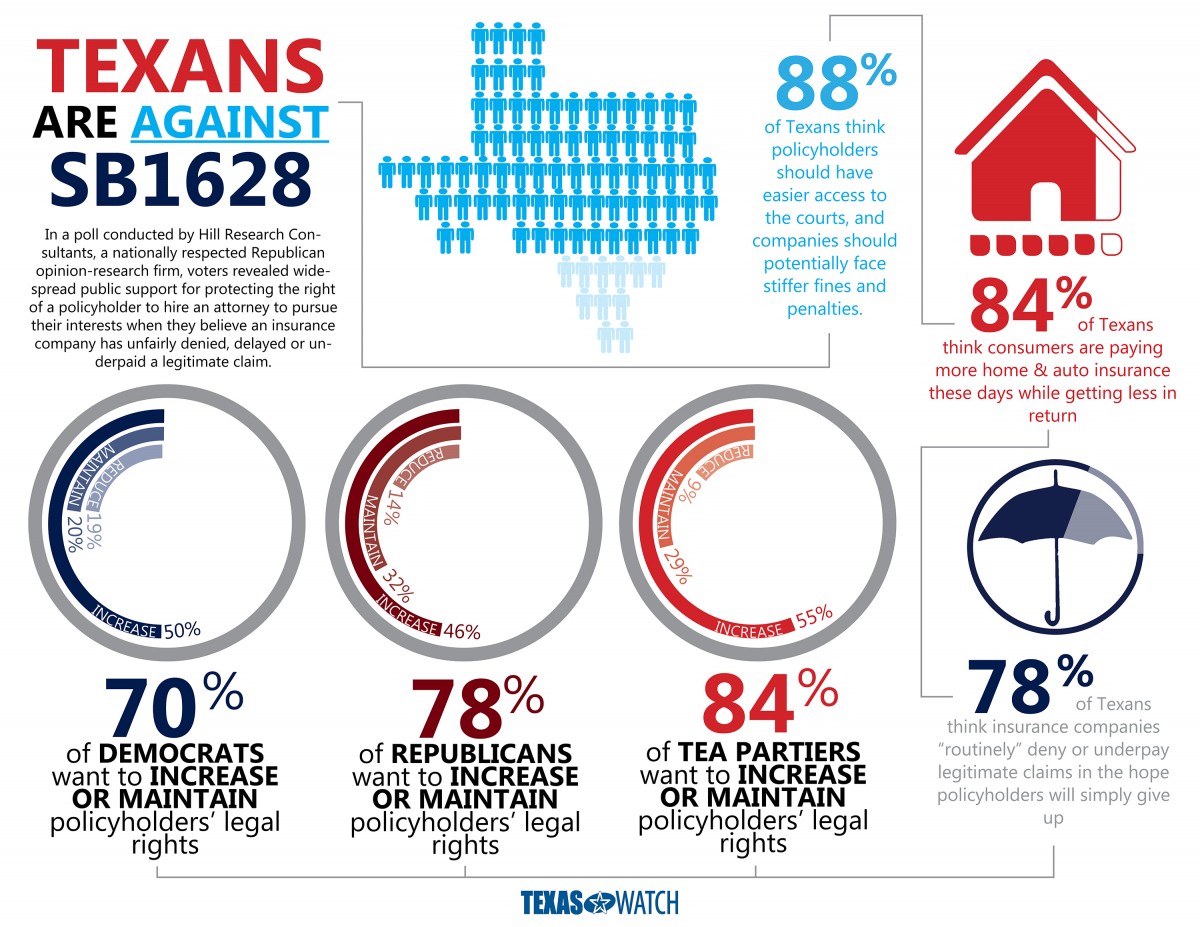

Proponents of SB 1628 know that they cannot defend this bill on its merits. It speaks volumes that rather than debate the merits of the bill, they are making personal attacks.

With growing opposition within the business community and a grassroots groundswell of opposition from Texans all across the state, this attack smacks of a desperate attempt by a lawmaker and lobbyists trying to save their bill. The bottom line is that Texans don’t want this.

{kind=link}

We won’t be distracted by mudslinging. Our focus is on the real-world detrimental impact this bill would have on Texas families and businesses.

Senator Taylor is selling a line that his bill somehow helps consumers. You don’t help policyholders by taking away their rights. The policyholder protections that have been on the books for over 40 years are the last line of defense between Texans and the greed of the insurance industry.

The facts about SB 1628’s impact on commercial and individual policyholders are these:

- Hollowed out damages: A right without a remedy is no right at all. CSSB 1628 fatally defines the term “actual damages” downward, removing wrongfully withheld policy benefits from the recoverable damages for all policyholders under Ch. 541 (Section 2). Policy benefits, of course, form the bulk of a policyholder’s damages. CSSB 1628 also undermines Ch. 542 by only allowing policyholders to recover interest on the unpaid amount of the claim (Section 10), which incentivizes low-balling by insurers. If an insurer offers to pay 75 cents on the dollar, you can’t put on 75% of a roof. The policyholder either has enough money to make the necessary repairs, or the repairs can’t be made. Homeowners can’t rebuild, businesses can’t reopen, and people can’t return to their jobs.

- Expanded immunity: Under CSSB 1628, employees, agents, representatives, and adjusters can all be immunized (Sections 3). Currently, these people must follow the law when investigating, adjusting, and paying claims, which means they owe a statutory duty to policyholders. Under this change, they may act without personal consequence, meaning their financial relationships with insurers will control their findings and dealings. This change will also have the effect of pushing insurance cases into federal courts, driving up litigation costs and delaying policyholder suits, which will be parked behind federal criminal trials. This would have the result of pressuring claimants into accepting low-ball settlements or risk waiting for years to have their case resolved. State law claims should stay in state court.

- Hard and short statute of limitations: All property damage claims would essentially be subject to a hard two-year statute of limitations, regardless of when the policyholder discovered – or should have discovered – the damage (Section 12). This change ignores the fact that certain structural damage and systems failures inside of walls, closets, and foundations can take time to detect.

- Frivolous defenses: Insurers already possess the ability to make qualifying offers of settlement and dismiss non-meritorious claims. However, under CSSB 1628, insurers will now be able to raise a number of new defenses, including a “bona fide dispute” trump card (Section 1) and a new “knowing” standard added to Ch. 542 (Section 10), as well as “gotcha” defenses through the outright dismissal of property claims on mere technicalities if policyholders do not comply with every last requirement of onerous new notice procedures (Sections 7, 8).

But, don’t take our word for it. Read the bill for yourself.